About the Author

Catherine Austin Fitts is president of Solari, Inc. Ms. Fitts served as Assistant Secretary of Housing during the first Bush Administration, lead financial advisor to the U.S. Department of Housing and Urban Development during the Clinton Administration and is a former managing director and member of the board of Dillon, Read & Co. Inc. Biographical information.

Catherine Austin Fitts is president of Solari, Inc. Ms. Fitts served as Assistant Secretary of Housing during the first Bush Administration, lead financial advisor to the U.S. Department of Housing and Urban Development during the Clinton Administration and is a former managing director and member of the board of Dillon, Read & Co. Inc. Biographical information.

Summary

Media revelations are unfolding daily regarding losses in the U.S. mortgage market. These losses are not a new phenomenon. Rather, they represent the latest phase in an ongoing tradition of institutionalized fraud in the U.S. mortgage system and the federal credit system that directly and indirectly guarantees it. An understanding of this history can mobilize public support for reforms that address root causes by reversing the profitability enjoyed by those responsible.

Where is the Money? Let’s Get it Back!

by Catherine Austin Fitts

Republished Article

Original (5 Nov 2008)

Large banks now claim recent losses in the US mortgage market totaling over $100 billion. While amounting to only a small percentage of banking profits over the last decade, this is still a lot of money. It may pale by comparison,  however, to the losses the banks’ customers, the communities drained by predatory lending and investment practices and the citizens who stand behind the federal credit may incur.

however, to the losses the banks’ customers, the communities drained by predatory lending and investment practices and the citizens who stand behind the federal credit may incur.

Municipalities from Australia to Montana are reporting losses on U.S. mortgage and structured investments sold to them by the banks. (1) (2) Just as small towns in the Norwegian Arctic Circle reported losses of $167 million on investments packaged by Citicorp, Citicorp’s departing CEO exited his job with a $100 million compensation package.

The City of Baltimore is suing Wells Fargo. The City of Cleveland is suing them as well, as part of the city’s suit against 21 Wall Street banks, a veritable who’s who of U.S. mortgage lending and securities, including JP Morgan Chase, Citicorp and Goldman Sachs, arguably the most prestigious member banks of the New York Federal Reserve Bank, the depository for the U.S. government.

According to the Baltimore lawsuit, nearly 450,000 properties were in some stage of foreclosure during the third quarter of 2007. The Baltimore lawsuit cites a recent study of Chicago communities in which it was estimated that each foreclosure is responsible for an average decline of approximately 1% in value of each single-family home within a quarter of a mile.

While the financial community holds its breath waiting for pension fund annual reports to disclose what may be the most significant losses, the stock market continues to drop, evaporating the wealth of millions of investors in America and around the world.

The state pension fund lawsuits over stock portfolio losses have begun. The Ohio Public Employees Retirement System is suing Freddie Mac, and Norfolk County Retirement and the New York City and State Pension Funds are suing Countrywide. Ultimately, pension stock portfolio losses will be insignificant compared to the fixed income portfolio losses expected to wipe out billions in retirement savings.

The state pension fund lawsuits over stock portfolio losses have begun. The Ohio Public Employees Retirement System is suing Freddie Mac, and Norfolk County Retirement and the New York City and State Pension Funds are suing Countrywide. Ultimately, pension stock portfolio losses will be insignificant compared to the fixed income portfolio losses expected to wipe out billions in retirement savings.

The last time the U.S. media exposed mortgage fraud of this magnitude was in 1989. In April of that year, I was appointed Assistant Secretary of Housing/FHA Commissioner at the U.S. Department of Housing and Urban Development (HUD) only to find that the FHA single family mortgage insurance fund, required by law to be financially sustainable, was losing $11 MM a day and that the combined FHA mortgage insurance funds had lost $2 billion in the Texas region alone over the prior year. The mortgage fraud at HUD, one of the largest issuers of mortgage securities in the world, was so bad that Secretary of Treasury Nicholas Brady privately tried to dissuade me from joining the agency, saying “You can’t go to HUD — HUD is a sewer.”

The HUD losses were a drop in the bucket compared to the losses on the savings and loan institutions, ultimately costing U.S. taxpayers an estimated $500 billion by the time the clean-up was through in the mid 90’s. This estimate did not include the subtle and more expensive inflation borne by ordinary citizens, resulting from allowing the large financial institutions to use the federal credit to borrow inexpensively in the short-term markets and reinvest in long-term U.S. Treasury and agency securities, helping some of them dig out of the losses and resulting in windfall profits to the industry across the board.

Policymakers encouraged those of us leading the last clean-up to fashion reforms such that mortgage fraud on this systemic scale “could never happen again.” And so significant financial reforms were legislated and instituted.

First and foremost, were laws requiring federal agencies and credit programs to produce audited financial statements. As a significant amount of the US mortgage market enjoys direct or indirect support of federal credit programs, such an audit requirement should ensure that any problems in the housing finance system are illuminated early on. Part of this reform, so-called “paygo,” (The equivalent of “loan loss reserves” required of private lenders) would make it prohibitively expensive for Congress to extend federal credit to support a new bubble.

Second, were administrative steps to ensure transparency of federal mortgage credit and spending by county and zip code. The most effective internal control is knowledgeable citizens, watching the use of government resources on their home turf. With easy access to data about government resources expended locally, communities could assess the performance of their tax-supported housing and mortgage resources contiguous to the areas in which they live, work and vote for political representation. Without access to such “place based” financial information, it is difficult to hold our legislative representatives accountable.

What happened? Beginning in 1995, numerous government agencies and the US Treasury began annual announcements declining to publish audited financial statements. In the process of explaining itself, HUD announced “undocumentable adjustments” to balance its books in 1998 and 1999 of $17 billion and $59 billion, declining to give a total for the undocumentable adjustments in 2000. In the process, the Office of Management and Budget solved the loan loss reserve problem by cooking the assumptions used to estimate costs, thus permitting issuance of greater amounts of mortgage credit with lax terms and conditions. Things got so bad that the chief of staff to the chair of the Senate Appropriations Subcommittee in 2000 confessed to me “HUD is being run as a criminal enterprise.” The myths that there was a budget surplus during the Clinton Administration or that the housing bubble began after the Clintons left office represent the partisan fantasies of Americans desperately searching for ways to avoid facing the real risks before us.

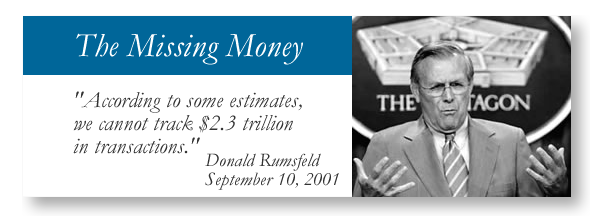

Even more money was missing at the Department of Defense (DOD). On September 10, 2001, Secretary of Defense Donald Rumsfeld conceded, “According to some estimates, we cannot track $2.3 trillion in transactions.”

By 2003, more than $4 trillion of “undocumentable adjustments” had been reported at HUD, DOD and NASA alone. Since then the federal government fails to account for additional billions each year as the U.S. commitment in Iraq leads to unprecedented spending with third party contractors, many under “no bid” contracts and without meaningful contracting supervision. Finally, after years of manipulation in the precious metals markets, serious concerns are growing about the status of the US gold stores. Has our gold gone missing as well?

In the 2007 Financial Report, the U.S. Comptroller General stated “Certain material weaknesses in financial reporting and other limitations on the scope of our work resulted in conditions that, for the 11th consecutive year, prevented us from expressing an opinion on the financial statements…”

In the 2007 Financial Report, the U.S. Comptroller General stated “Certain material weaknesses in financial reporting and other limitations on the scope of our work resulted in conditions that, for the 11th consecutive year, prevented us from expressing an opinion on the financial statements…”

Meantime, efforts to bring local transparency to government mortgage programs and credit have been stopped, destroyed or reduced to ineffective window dressing. (See articles: Where is the Collateral? and So, Where is the Collateral?.) The average American has little understanding of the government resources and credit programs around them.

So our earlier reforms failed to prevent billions in subsequent mortgage fraud losses and the disappearance of trillions from US government accounts. Why? What have we learned from this failure, which would suggest lasting reforms?

If your public company were operating outside its bylaws and U.S. Securities and Exchange Commission regulations requiring audited financial statements, at some point your bank would refuse to effect your banking transactions and stop selling your securities to their customers. This means if $4 trillion is missing from the U.S. government, the federal depository and its member banks are complicit, if not responsible.

We don’t need new laws for each new crisis. We need enforcement of existing laws. What we also don’t need are bank depositories and government payment and accounting contractors who will proceed with trillions of banking transactions and government securities sales while basic provisions of the U.S. constitution and laws governing federal financial management are blatantly ignored.

In 1989, we failed to identify what money, credit and assets had been stolen and to get them back.  Billions of dollars in profits remained in the pockets of the conspirators and their co-conspirators – the investors, strategic partners and offshore backers to whom they funneled it. Rather than hold people and institutions accountable and achieve restitution, we plowed additional back door profits into the financial institutions and allowed them to continue in their role as member banks and shareholders of the New York Federal Reserve Bank, depository to the US Treasury.

Billions of dollars in profits remained in the pockets of the conspirators and their co-conspirators – the investors, strategic partners and offshore backers to whom they funneled it. Rather than hold people and institutions accountable and achieve restitution, we plowed additional back door profits into the financial institutions and allowed them to continue in their role as member banks and shareholders of the New York Federal Reserve Bank, depository to the US Treasury.

These institutions continued to provide a wide number of important services to federal, state and local government and pension funds, ensuring their access to extraordinary amounts of revenues, assets and critical inside market information. We continued to accord them, their investors and the politicians they funded the prestige and power traditionally reserved for a society’s most trusted stewards and fiduciaries. By so doing, we legitimized and institutionalized mortgage and financial fraudsters on a global scale. (1) (2) (3)

Trillions of dollars are missing. Where did it go? Who has it? Let’s act on what we learned the last time around – “Crime that pays is crime that stays.” This time, let’s ask and answer the right question: “Where is the money and how do we get it back?”

The Fed’s War on the Middle Class

Mises Daily by Mark Thornton | Posted on 6/4/2008 12:00:00 AM

http://mises.org/story/2983

I think we going to revert to barter system soon. So if you’re not standing behind anything valuable, sorry.

Money –$$, gold, etc– is a consenual illusion. The stuff of muysticism & Wizards, accepted becausewe all “believe” in it, including most Wallstreeters. Not all. Here’s the test: not “precious metals,” but Reality vs Mind-constructs: think 1st of what 10 things y9ou cannot LIVE without. Neither money nor oil will be there if you’re saqne. You need: air, drinkable water, a habitable environment (temperature, shelter?) and food. Arguably, love & touch. Perhaps you could add, grass, trees, soil — since these provide the food & air. Money isn’t even there. Here’s test two: imagine, through some catastrophe, all human consciousness has vanished from this planet. What remains?? The earth remains, the biosphere, the wind and ice and animals. Some of the poisons are left over, but they degrade, the cities crumble into elements. Life can still remain; there could still be animals, which means sentience isn’t erased. But the madness that governs human society — the part called “civilization, Western, late-p-” is gone; the good with the bad. THe Theocrats will say God remains; the question for them is, does that imply corporations & inbstruments of legal tender? Of course not. In Xtian terms, they have set up the haven of the money lender. I would say to Christians, assume Christ is your winning quarterback & due to injury he’s out for the Big Game. YOU have to go in, & call down the MONeyLender & all his instruments. This is not an anti-Semitic diatribe; no one people should be blamed. Money may begin as a Babylonian or Middle Eastern Story, but we have only to recognize it as the $tory we tell ourselves (illusion), and say, we will no longer trade breath & earth for the MOneyleners’ fictions. We have the right to do that, we can be gentle, we needn’t kill anyone. Leave the rich their houses– one house — let them live out their lives. Spit on no one; we are all subject to Illusion. The point is, to get free, to wake up & breathe air before Methane & the Benzene Ring — the true six-sided serpent (no, I’m not a mystic: check the history of the man who discovered the structure of the Benzene Molecule — he dreamed a 6-sided serpent with her tail in her mouth, promising unlimited power. That’s scary, and we old Icelandics know: no power is for free. The cost, this time aroiund, for unlkimited POWER for a few, is the breath of Life, and earth.

I wish I could find good posts like yours more often. It was a pleasure to read.

It’s all such a universal joke. Money. The question isn’t where is it but what is it?

The paper everyone mutually agrees, by lack of an alternative choice, to is forced upon us. It is by our unconscious reason we call it “money”.

The concept of money is fine but the ignorant masses have been slowly conned away from us retaining it’s value, which should reflect a fair tradable value for what we have done to “earn” it.

Currently a perfect example of the con is how there is a flood of new coins, U.S. passing hands in everyday consummer commerce. Most of which should be concidered false money. Such the new dollar coin that bears a “gold” appearance. Yet no one asks why. It’s not gold. Why should it be given that appearance if not to deceive the unwarry. It has no numismatic value, really. There is also the new state coins, quarters. lots of people collect them. Why can be nothing more than for memrabilic tokens, like street car tokens from a by gone era.

Well the con is this I believe. For the mass of immegrants that come to the US, they bring with themselves a false impression as to “how America is” V.S. what it was. From Mexico to the middle east most nieve ones have the impression it’s still in the ’50’s. And that the U.S. streets are easy to get work and aquire the American dream from. That is until they stay a few years. But their accepatnce of the coins and money as is, is ignorant to what it represents. That is a depreciating transfer of vanishing value.

Therefore they accept it as having some intrinsic value like gold or silver. My god the pennies aren’t even copper any more. SO one can’t even save pennies for their copper value. But we can strip buildings of the copper pipe and wires!

I can go on an on regarding the CON. But I wont. here is one last thought. Again, What is money? When it is said Gold costs are up or eggs or Euro’s ….the key word is “Cost”. That is relative to what? Fiat money? Notes? I,O,U’s ? They are all the same thing. A supposed prmise to pay…….something for the wanted item. My I.O.U. is as good as gold. But golds value, ehem, to it’s self I suppose, is a constant the only thing that really changes is the worthlessness of the “money”.

So Katherine, we need not ask “what happened to the money”, but “where’s the gold, all of it?”

The big joke about it all is the Treasury or Federal Reserve, who ever prints up the notes, still prints “In God We Trust” on the paper notes, yet on the fake coins it doesn’t even say that.

I guess there is no one to trust any more.

Oh. news flash, for me. I just notice it does say In God WE Trust on the edge of those fake gold dollars. But still the edge is the first thing to wear out.

So just to close here’s just a little history of the “way” in which US coins look the way they do. Besides the fact that the CONstitution say “Only CONgress has the power to ‘coin’ money and regulated the value therof…” (it doesn’t say print it either) , Well, do you know that the “edge” on coins, that of silver or gold, where made with serrations, those little ribs, around the perimeter to guarantee that when you received them, you could be assured that you were receiving it’s full weight in the accepted precious metal they where made of ?

That ment that 1 ounce of gold or silver or purportion thereof , like Half a dolllar or quarter or dime, was it’s full weight backed by the United States of America.

Those little ribs around the edge were a deterrent to stop theives from going down in the basement and “milling off” a portion of your wealth.

So my question now is, “if the coinage of the realm has no precious value, why are the little ribs still there?

All I can assume is that it is a direct effort to deceive the people into believing and accepting the fake money for something of real value.

Sidebar: Those new fake gold coins have no edge ribbing. They do say though, “In God We Trust”.

Deductive reasoning therefore tells me, I can’t trust this shit any longer!

Anyway I hope you’ve learned something.

I know how to get the money back.

All of it and then some.

The same way the 14 people who were being foreclosed on in Ohio got their homes for the price of asking for the “original note” to be produced in order the bank may have standing in court.

What most people are not aware of is that all law in the USA is under the UCC and not constitutional law as many erroneously assume.

Until the average man in the street gets that through his skull everything, will be to his detriment.

We should never have stopped eating the missionaries and the salesmen that followed them.

What’s worse for the future of the planet; Consumerism or Cannibalism?

Part of the mechanism which is used is the myth of Middle Class. The Middle Class were the lords of manor who were between the peasants and the Royals. Either you are working for your next meal or you are not. That’s feudalism, and it’s what we have. The sooner we realize that all those ‘retirement plans’ and ‘vacations’ are just distractions from real life, the better off we will be in our gardens. The rich are just tagging along on this Gravy Train, and it’s time we pulled the pins to their caboose and left them to rot. We don’t need them, we don’t need their ‘advice’, and we don’t need their train. Buy local, live local. The land and the people will go on.

Collapse? Bring it on.

http://www.whatawaytogomovie.com

A plan hatched at the Bohemain Grove no doubt. Thanks for shedding insider light on this. I think there is a surprisingly large movement afoot that understands (finally) the incredible manipulation by he financial institutions and the elite that control them (geez it’s only been going on since, what, 1913!) This to me is nothing but pure thinning of the herd…too many millionaires interfering with the billionaire’s plans. Too many resources being used up too quickly by the rest of us, so drive up prices, drive up oil, reduce the spending power of the dollar, reduce the value of our assets and sit back and laugh (all the way to the bank). Anyone wonder why the gold reserves were being heisted out of the basement of the WTC on 9/11? Lots of dots to connect here but not too hard to figure out who is behind it all, they are pretty flaunting it now.

peace

I have long asserted that this “subprime mortgage” thing was just another way to suck money out of ordinary people’s wallets by leveraging their greed. The question I have is this: if money is lost by the persons in foreclosure (it is), money is lost by the affected communities in lowered tax base and increased criminal activities Iit is), money is lost by the investors backing these mortgages (it is), money is lost by the foreclosing institutions (it seems to be)…and money should be a zero-sum game…where is the “lost” money going? Somebody’s making a killing off of this, the question is WHO and how are they making it look like the money is just evaporating?

Alternatively, is it possible that these instruments were never in real money to begin with, and if so, how can we tell what IS real? Gold?

I don’t think so…based on behaviors and hype, I increasingly feel that the precious metals markets, particularly gold, are under the same manipulation, and that they will peak and crater soon, sucking even more money out investor’s pockets. I see us being “herded” from one “safe” investment (mortgages) to another (gold)…and it’s just a one-two punch waiting to happen.

I’m curious if other people are perceiving something similar.

I wish to simply thank you for everything you have done to help”the people” of the United States.Too often,those who have your back round,as well as status in our society forget the meaning of civic responsibility as well as forgeting that there ,but for the grace of god,walk I.From the bottom of my heart.Thank you for what you have done.

Much of what you have shown the world I was aware of,but the way you have presented this information is comprehensive,and clear enough for even a layman to grasp.This is a excellent example of what happens when the foxes run the chicken house.In this case,the thieves run the bank Once again thank you.